When you think of retirement savings, most of the focus goes to contributions and investment returns. But there’s a quieter, less visible factor that makes a massive difference over time: fees.

Every retirement account – 401(k), IRA, annuity, pension, mutual fund, or ETF – comes with overhead costs. These fees may seem small at first glance, but they’re charged every year on your entire balance, which means they compound against you.

Let’s break down what you’re really paying, why it matters, and how to keep more of your money working for your future.

IMPORTANT: Not all fees are bad – some are necessary if you want professional management, guidance, or convenience. There is nothing wrong with a hands off approach. The key is knowing what you’re paying for.

Why Fees Matter

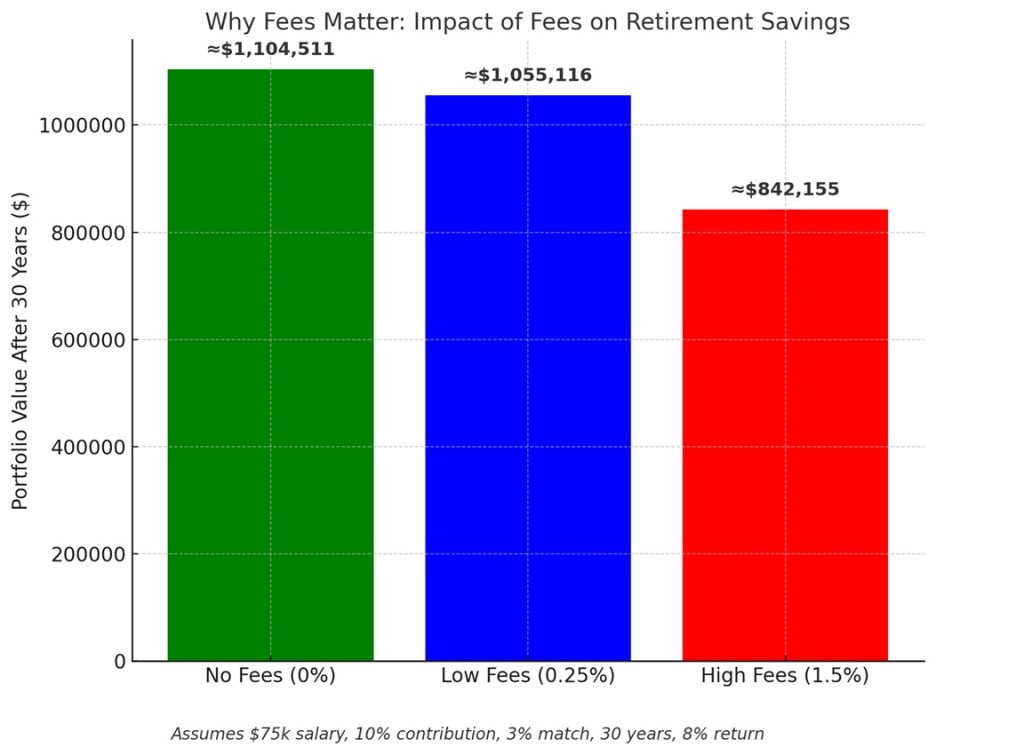

Here’s a simple example:

- Salary: $75,000/year

- Contribution: 10% ($7,500/year)

- Employer match: 3% ($2,250/year)

- Timeframe: 30 years

- Growth assumption: 8% annual return

No Fees (0%) → ≈ $1,104,500

Low Fees (0.25%) → ≈ $1,055,100

High Fees (1.5%) → ≈ $842,200

That’s $262,300 lost to fees – money that could have been yours.

Just like investment returns compound in your favor, fees compound against you.

Fees by Investment Type (with Descriptions)

401(k) Plans

Employer-sponsored plans offer convenience and company matches, but they come with layered fees.

- Administrative Fees (0.2%–1% or $20–$200 annually): Cover recordkeeping, compliance testing, statements, and customer service.

- Investment Fees (0.03%–1.5%+): Expense ratios for funds inside your plan; index funds cost less, active funds more.

- Managed Account Fees (0.5%–1%): Charged if you pay for “professional management” of your 401(k).

- Service Fees ($50–$200): Applied for optional actions like loans, hardship withdrawals, or QDROs.

Roth IRAs

You have more control over what you invest in with a Roth IRA, and fees tend to be lower.

- Account Fees ($0–$50 annually): Some custodians charge maintenance, though many brokers now waive these.

- Investment Fees (0.03%–0.2% for ETFs; 0.5%–2% for mutual funds): Expense ratios for your chosen investments.

- Transaction Fees ($0–$20 per trade): Charged when buying or selling, though commission-free options are common.

- Advisory Fees (0.25%–1%): If you use a robo-advisor or personal advisor to manage your IRA.

Annuities

Annuities are insurance products that guarantee income but often stack on fees.

- Mortality & Expense (M&E) Fees (0.5%–1.5%): Pay for the insurance guarantees, like death benefits.

- Administrative Fees ($30–$100 annually): For recordkeeping and servicing.

- Investment Management Fees (0.5%–2%): If your annuity uses sub-accounts that act like mutual funds.

- Rider Fees (0.5%–1.5%): Optional add-ons for benefits like guaranteed lifetime income.

- Surrender Charges (5%–10%): Penalties if you withdraw early.

Pensions

Pensions hide most fees because employers cover much of the cost, but they still exist.

- Administrative Fees (0.1%–0.5% or $50–$200): For plan operation, actuarial services, and statements.

- Investment Fees (0.5%–2%): Deducted indirectly through fund expense ratios.

- Advisory Fees (0.5%–1%): If employees opt for financial planning services.

Mutual Funds

Mutual funds are one of the most common investments, but also one of the trickiest when it comes to hidden fees.

- Expense Ratios (0.03%–2%): Cover fund management salaries, operations, and research.

- 12b-1 Fees (up to 1%): Marketing/distribution costs, often unnecessary.

- Load Fees (1%–5%): Sales charges when you buy (front-end) or sell (back-end) shares.

- Transaction/Redemption Fees ($10–$75 per trade, or 0.5%–2%): Extra costs for short holding periods or broker transactions.

ETFs

ETFs are generally cheaper than mutual funds and easier to access.

- Expense Ratios (0.03%–0.7%): Cover management of the fund; index ETFs are especially cheap.

- Trading Commissions ($0–$20 per trade): Most brokers now offer commission-free ETFs.

- Bid-Ask Spread (0.01%–0.5%): Hidden cost of buying at a slightly higher price and selling at a slightly lower price.

Additional Realities About Fees

- Fees compound too: Just like your investments grow, so do the dollar amounts you pay in fees as your balance grows.

- Actively managed vs. passive funds: Passively managed index funds and ETFs usually charge much less (0.05% is realistic) than actively managed funds.

- Advisor fees stack: Managed accounts within a 401(k) may charge 0.5%–1% in addition to the underlying fund expenses. Working with a financial advisor may add another 0.4%–0.6%.

How to Check Your Fees

Understanding what you’re paying isn’t always straightforward, but here’s how you can uncover the true costs in different types of accounts:

401(k) Plans

- Log in to your provider’s website: Look under Documents or Plan Information. Most providers host all disclosures here.

- Annual Participant Fee Disclosure (404(a)(5)): By law, your plan administrator must send this at least once every 14 months. It details plan administration fees and investment expenses.

- Quarterly Statements: Review them for direct fees like administrative charges.

- Fund Expense Ratios: Use the ticker symbol of each fund in your 401(k) to look up its expense ratio online or on your provider’s portal.

- Fund Prospectus: Each investment option includes a prospectus with the official breakdown of costs.

- Third-Party Tools: Services online can help analyze hidden fees in retirement accounts.

IRAs, Mutual Funds & ETFs

- Brokerage Account Portal: Most brokerages list the “expense ratio” next to each fund in your account.

- Fund Prospectus: Always the most accurate source for expenses.

- Financial Websites: Platforms like Morningstar or Yahoo Finance let you plug in a fund’s ticker symbol to see its fees.

- Statements: Check for transaction fees if you’re trading individual ETFs or mutual funds.

Annuities

- Contract Documents: Carefully read the fine print, especially for rider fees and surrender charges.

- Annual Reports or Statements: These may summarize ongoing M&E (mortality & expense) charges and investment subaccount costs.

- Ask the Provider Directly: Annuity contracts can be complex, so don’t hesitate to request a full fee breakdown.

Pensions

- Plan Administrator or HR: Request fee disclosure documents.

- Plan Booklet (SPD): The Summary Plan Description should outline administrative and management costs.

- Trustee/Recordkeeping Disclosures: Some pensions list these separately, so it’s worth asking.

What You Can Do About Fees

- Choose low-cost funds: Index funds and ETFs often charge a fraction of what active funds do.

- Avoid unnecessary add-ons: Skip managed account services or costly riders if you don’t need them.

- Use commission-free platforms: Many brokers now let you trade ETFs and stocks without transaction fees.

- Consolidate accounts: Fewer accounts means fewer administrative charges.

Why Still Use a 401(k)?

This post isn’t meant to scare you away from investing. In fact, it’s the opposite – even with higher fees, 401(k)s still offer significant advantages.

- Employer match = free money: Any match is an instant 100% return on that contribution.

- Payroll automation: Contributions happen before you even see the money, helping you stay consistent.

- Tax advantages: Traditional 401(k)s lower taxable income now, while Roth 401(k)s grow tax-free.

The bottom line: don’t abandon your 401(k) – but do pay attention to fees. The less you pay, the more you keep.

Remember: pay for value, not waste. The right fees can support your growth, but hidden ones can quietly hold you back.

Knowledge is power. The more you understand your fees, the more you can take control of your financial future. Review your accounts, know what you’re paying, and make sure your hard-earned money is working for you – not against you.

Leave a comment